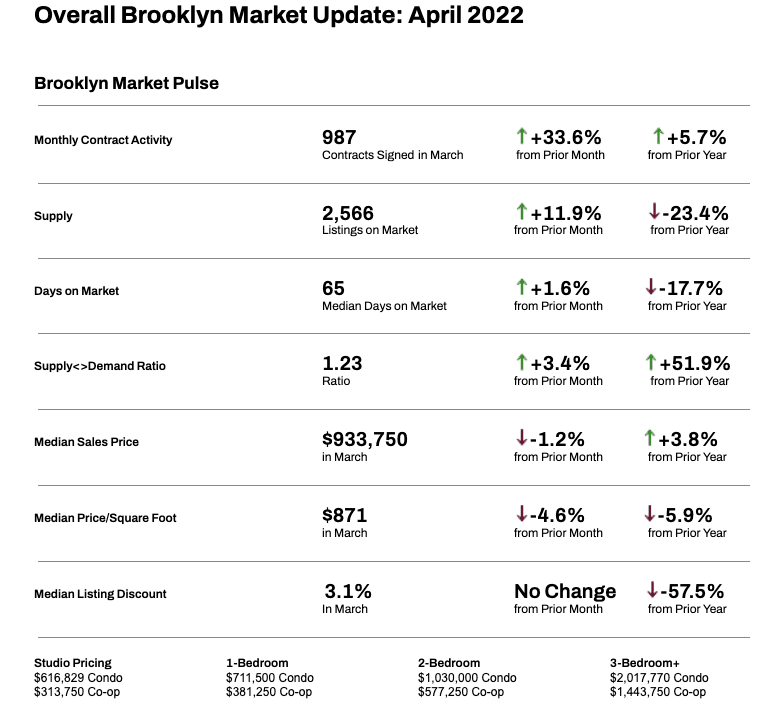

Brooklyn Market Update

Rounding out Q1 2022, Brooklyn contract activity popped in March with 987 contracts signed, a 34% increase from February. More sellers have listed, to meet the persistent demand, with 1,340 new-to-market homes increasing overall supply by 12% compared to March to 2,566 homes available for sale. While demand is up 6% year-over-year, supply is down 24% in the same time period, which has led the Market Pulse to increase 52% over the same time period to 1.23, indicating a very strong seller’s market. The median listing discount held steady at 3.1%, the same as February, and a decrease of 57% since the same time in 2021. The median sales price dropped 1% since February and increased nearly 4% in the last year. Homes are still trading quickly, entering contract within 65 days on median, 1.5% slower than last month and 18% quicker than last year. Increasing interest rates, which are rising at the fastest rate in decades, are accelerating some buyer demand. Coupled with headlines pronouncing the continued strength of the Brooklyn real estate market — and the resurgence of NYC coming out of COVID — buyers may be having a FOMO moment and feeling intrinsic and extrinsic pressure to transact sooner.

Brooklyn Supply increased by 12% compared to February, bringing the total supply to 2,566 units for sale. In March, 1,340 new listings came to market, 52% more than February and 1.5% more than last March. Supply currently stands 23% lower than the same time last year, which coupled with increased demand, has driven the Market Pulse Higher, indicating a more competitive market for buyers.

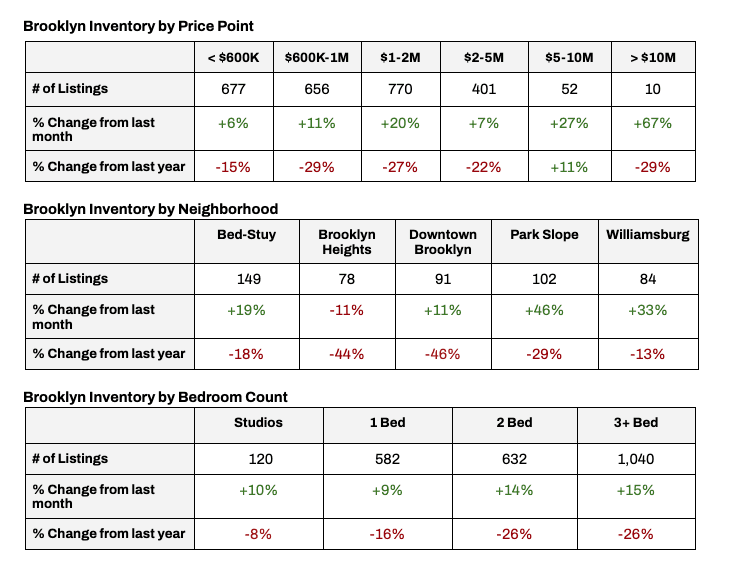

INVENTORY: Key Takeaways

- In the last month, supply increased across all price points, neighborhoods and sizes, with the exception of Brooklyn Heights.

- Supply increased the most in Park Slope and Williamsburg, up 46% and 33% respectively in the last month.

- Two and three bedroom homes saw the largest percentage increase in March, up 14% and 15% respectively.

- In the last year, supply has decreased across all price ranges, neighborhoods and home sizes except for those priced $5–10M.

Brooklyn Buyer Activity, as measured by signed contracts, increased 34% compared to February with 987 contracts signed in March. Compared to March 2021, 6% more contracts were signed this year.

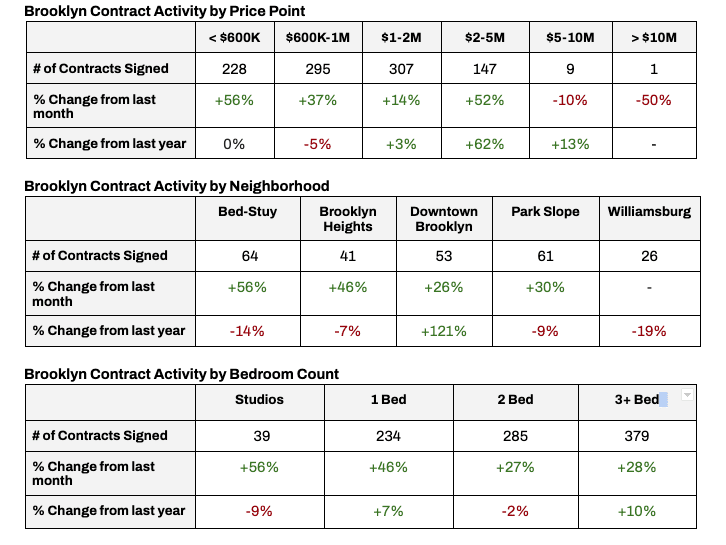

CONTRACT ACTIVITY: Key Takeaways

- In the last month, contract activity increased across all price ranges, neighborhoods and sizes, except for the $5-$10M and $10M+ price ranges.

- Bed-Stuy and Brooklyn Heights saw a large boost in contract activity in the last month, up 56% and 46% respectively.

- Contract activity increased more than 50% for homes priced under $600K and between $2–5M in the last month.

- In the last year, Downtown Brooklyn saw a 121% increase in contract activity and homes priced $2–5M saw a 62% increase in contract activity in the same time period.

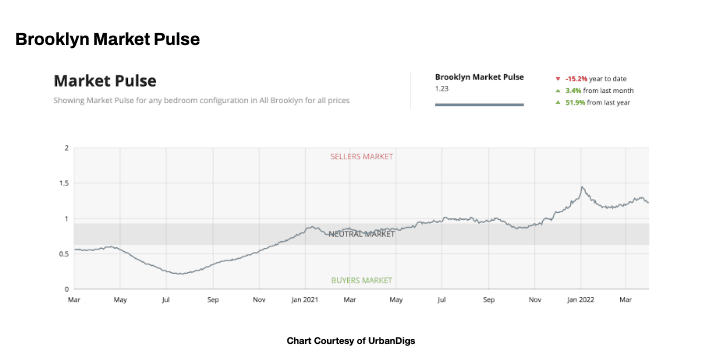

Despite an increase in supply, contract activity continued to increase at a faster pace in March, elevating the Market Pulse to 1.23, reflecting the continued strength of the current seller’s market in Brooklyn.

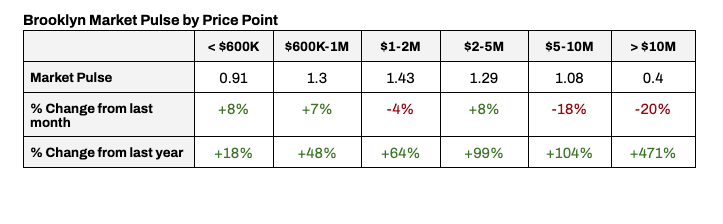

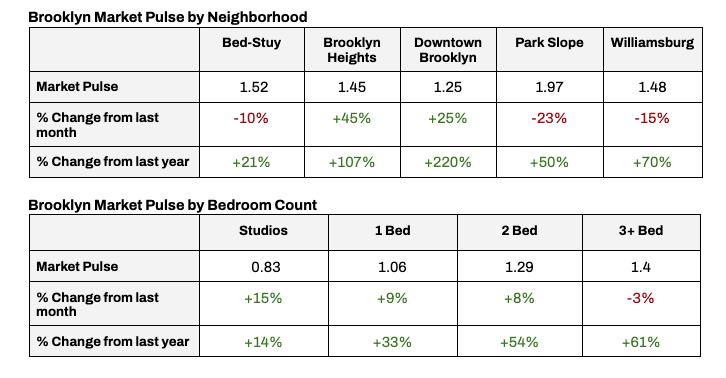

The Market Pulse [a ratio between pending sales and supply] is an indicator of leverage between buyers and sellers. A Market Pulse below 0.4 is considered a buyer’s market, a Market Pulse between 0.4 and 0.6 is considered a neutral market and a Market Pulse above 0.6 is considered a seller’s market.

MARKET PULSE: Key Takeaways

- The Market Pulse has increased the most, on a percentage basis, in Brooklyn Heights and Downtown Brooklyn to 1.45 and 1.25 respectively.

- Park Slope, which has long-had the highest Market Pulse in Brooklyn, saw its Market Pulse decrease by 23% to 1.97 as inventory rose at a faster pace than contract activity in March.

- While the Market Pulse is highest for the larger units [2 and 3-bedroom], in a departure from recent months, the Market Pulse increased at a faster percentage for studios and 1-bedrooms.

Pricing & Discounts

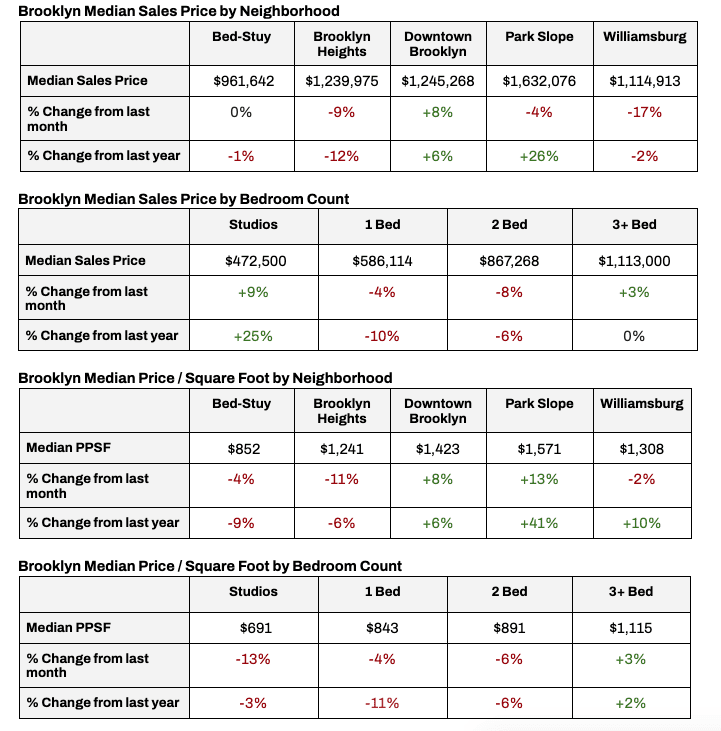

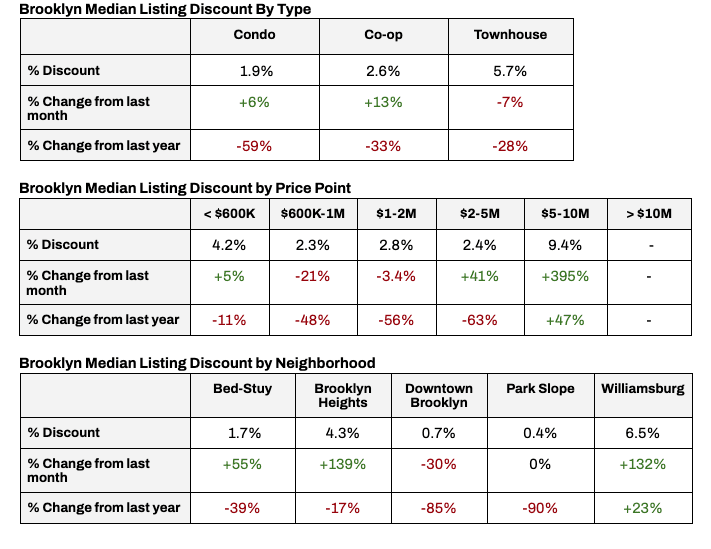

The Median Sales Price in Brooklyn decreased 1% from last month and increased 4% from last year to $933,750 On a price per square foot [PPSF] basis, the median decreased by 4.6% from last month and decreased 6% from the previous year, to $871. Meanwhile, the median listing discount remained flat from last month, at 3.1%, which is 57.5% lower than last year.

PRICING: Key Takeaways

- In the last month, Downtown Brooklyn was the one neighborhood to see an increase in median sales price, up 8% to $1,245,268.

- The Median sales price decreased for 1 and 2-bedroom homes, while it increased for studio and 3+ bedroom homes.

- Downtown Brooklyn and Park Slope have the highest median price per square foot, and were the two neighborhoods to see an increase in the last month.

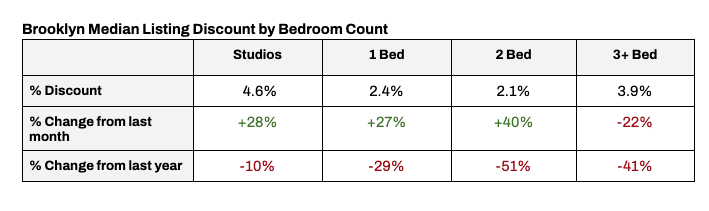

MEDIAN LISTING DISCOUNT: Key Takeaways

- Brooklyn condos continue to have the lowest median listing discount of the building types, but have seen more negotiability compared to February.

- The median listing discount has decreased for homes priced $600K-$1M and $1–2M, but has increased for other price ranges.

- Negotiability decreased in Downtown Brooklyn, increased in Bed-Stuy, Brooklyn Heights and Williamsburg and remained the same in Park Slope compared to February.

- In March, discounts decreased for 3+ bedroom homes and increased for smaller homes.

What this means for…

Buyers:

- Buyers are facing compounding pressure, from rising mortgage interest rates, stable prices, limited inventory and continued strong buyer demand.

- Mortgage rates are increasing at the fastest pace in decades, accelerating the plans for some buyers.

- Ample new supply is coming on the market this spring, offering new options for buyers, and buyers need to be ready to compete with other ready-to-transact buyers.

- Given rising rents and current inflation, with a holding period of 3–5 [or more] years, buying may make more sense than renting today.

Sellers:

- Rising new supply is increasing competition amongst sellers for buyers.

- Sellers need to read the market cues and readjust quickly if they are overpriced or mispositioned in the market

- Today presents a window of opportunity for sellers to come to market to take advantage of a confluence of market conditions creating pressure for buyers to transact sooner than later.

Renters:

- Covid-era rent discounts are a thing of the past, as renters experience rapid price increases which are erasing prior discounts and landlord concessions.

- Rents are now back in-line with the increasing trend of the last 5-years.

- Competition remains fierce amongst tenants, with apartments often receiving multiple offers and frequently going to bidding wars.

- Supply continues to trend downward heading into the spring and summer rental market as tenants may choose to renew rather than compete in the competitive market and move.

Investors:

- Rising interest rates should have a more muted effect in Brooklyn, as Brooklyn is less leveraged than most of America, enabling the NYC market to withstand the pressures of ascending interest rates better than many other national markets.

- Leveraged investors, who have a lower interest rate locked in, stand to benefit from the inflationary pressures and rising rental rates. Those investors should continue to hold and experience rising cap rates in the years to come.

Please contact us if you would like to learn more.